…Governance Has a Job to Do

A pattern has become familiar enough to name. Headcount comes down. Strategic investment goes up. Leadership frames the combination as transformation. The market, at least initially, tends to agree.

Oracle’s recent reduction of thousands of positions in service of an accelerating infrastructure buildout is only the latest iteration. Meta, Microsoft, and a cohort of others have moved through similar sequences over the past several years, each pairing workforce reduction with forward-looking investment narratives. The specific rationale varies. The underlying structure does not. Labor is being converted into capital, and the conversion is being presented primarily as financial logic.

That framing is incomplete. And the incompleteness is not a communication problem. It is a governance problem.

The Decision Inside the Decision

When an organization reduces headcount to fund a strategic priority, it is not making one decision. It is making three, simultaneously, whether it acknowledges them or not.

First, it is asserting that the new investment will generate more value than the capability being retired. Second, it is asserting that the remaining organization can absorb the reduction and still operate safely and effectively. Third, it is asserting that the trust cost, with employees, customers, and counterparties, is an acceptable price for the intended return.

Organizations typically spend their communication energy on the first assertion. The investment thesis gets the roadshow. The second and third assertions are handled, if at all, through HR messaging and transition programs. This is not an oversight. It reflects where boards and senior leadership tend to direct scrutiny. Investment decisions carry financial models, scenario analyses, and return expectations. The organizational consequences of the reduction that funds the investment are typically described, not stress-tested.

The governance failure is not malice. It is category error. Leadership treats the workforce reduction as a funding mechanism and evaluates it on cost terms. The investment it funds is evaluated on return terms. Neither is evaluated on the terms that matter most to execution: what has this organization just made harder to do well, and what is the realistic capacity of the structure that remains?

Capability Is Not a Line Item

The distinction between removing cost and removing capability is where governance either earns its function or exposes its limits.

Some organizations do carry structures built for an earlier stage of growth. Redundant management layers, misaligned roles, and headcount attached to legacy processes that no longer serve the strategy are real phenomena. Removing them is not reckless. In some cases it is overdue. But that category of reduction is analytically distinct from removing operational depth to fund a forward investment, and the two are routinely conflated in both internal deliberation and external communication.

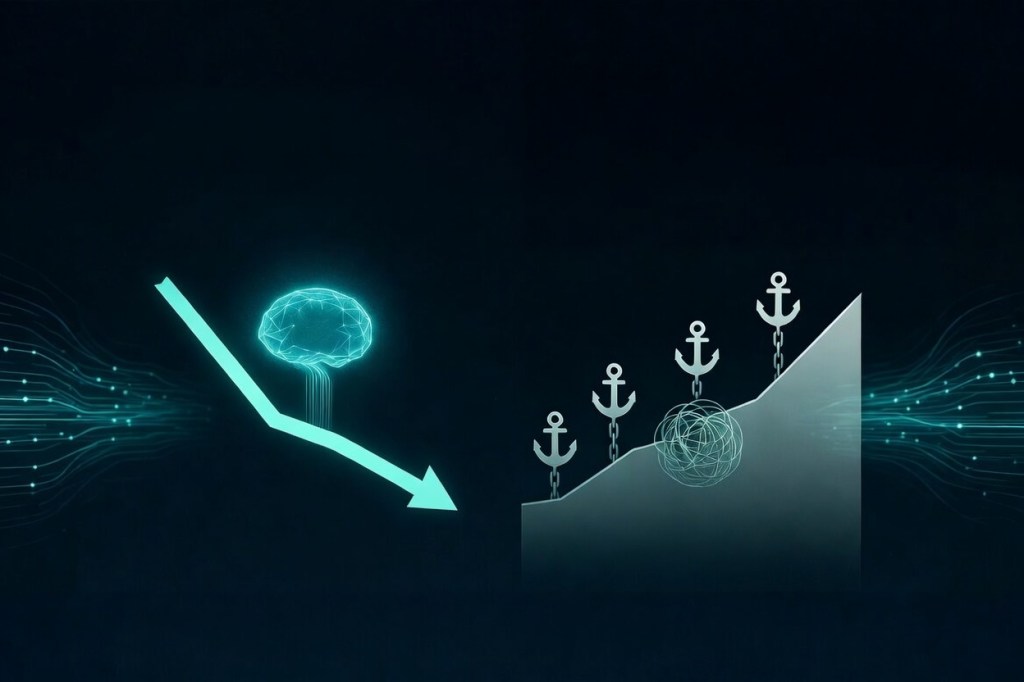

What gets retired when a company reduces operational headcount is not always visible in advance. Delivery continuity degrades when the people who understood how to navigate exceptions are no longer present. Escalation responsiveness suffers when management spans widen beyond the point where leaders can actually engage. Institutional judgment thins when the people who carried organizational memory and could recognize pattern-relevant risk leave or are pushed out. These are not soft outcomes. They are operating conditions, and they typically become visible only after the reduction has closed and the new investment is still in its early implementation phase.

The timing gap is structurally dangerous. The costs of the reduction arrive before the benefits of the investment. The organization is at its most operationally exposed precisely when leadership attention is most forward-directed.

Confidence as a Capital Allocation Question

Reframing the question helps clarify what governance is actually being asked to protect.

A workforce reduction funded by strategic investment is not only a financial reallocation. It is a confidence reallocation. The organization is betting that the remaining teams can still deliver to existing commitments while the new initiative builds toward its intended returns. It is betting that customers will not feel the operational thinning before the investment begins to produce visible benefit. It is betting that management has correctly estimated the execution depth required to absorb disruption without quietly degrading.

These are not HR questions. They are capital allocation questions, because they determine whether the investment being made actually lands in operating conditions capable of realizing its return. An investment thesis premised on an organization that cannot execute it is not a sound investment. It is a funding decision disconnected from operational reality.

Governance exists in part to hold that connection. Boards and oversight structures are positioned to ask questions that executive leadership, often proximate to the transformation narrative and accountable for its success, may not ask with sufficient rigor. The question is not whether the investment makes strategic sense. It is whether the organization executing it has the remaining depth to deliver.

What Governance Should Be Asking

The prescriptive case is not complicated, but it requires deliberate structure to execute.

Before approving a reduction-funded investment, governance should be able to answer whether the organization has modeled the capability consequence of the reduction, not just the cost consequence. That means identifying, specifically, which functions lose depth, which roles carry knowledge that is not documented or transferable on short timelines, and which operational buffers disappear when the headcount comes out.

Governance should also be asking about the timing exposure. If the investment takes eighteen months to produce operational return, and the reduction creates operational risk in months three through twelve, that gap is a contingency that belongs in the planning framework, not as an implicit assumption.

And governance should be asking about the trust trajectory. Employee confidence in organizational direction, customer confidence in delivery reliability, and counterparty confidence in institutional stability are not abstract values. They are execution prerequisites. A reduction that damages any of these ahead of the investment’s capacity to restore them creates a sequencing problem that no investment thesis resolves on its own.

None of this requires governance to be opposed to transformation. The question is not whether to reduce or whether to invest. Organizations frequently need to do both. The question is whether the combined decision has been evaluated at the level of rigor it demands, with accountability for the organizational consequences built into the approval, not deferred to implementation.

The Cost That Does Not Appear in the Model

Strategic investment does not exempt leadership from operational accountability. If anything, the commitment to transform raises the standard. Organizations that reduce in order to fund transformation are making a large, compounding bet: that the reduction was precise enough to preserve execution capacity, that the investment is sound enough to return more than the capability that was retired, and that the organization can hold together under the pressure of both simultaneously.

When that bet is made without adequate governance scrutiny of the operational consequences, organizations do not always become more efficient. They become more brittle. The transformation narrative continues. The dashboard shows investment progress. And somewhere in the operational layer, execution depth that was never modeled as a cost is quietly depleting.

That depletion eventually surfaces. It surfaces in delivery failures that seem disconnected from the reduction because the timing gap obscures the relationship. It surfaces in customer attrition that gets attributed to market conditions. It surfaces in management credibility erosion that looks like a leadership problem when it is actually a structural one.

The organizations that navigate this well are not the ones that avoid transformation. They are the ones whose governance asked, before the approvals were signed, what they were actually paying for the future they were buying. And held leadership accountable for that answer.

Version 1.1 — Updated March 2026